Summer 2025 Commentary

Market Recap

For the quarter ending June 30, 2025, U.S. stocks rose with the S&P 500 gaining 10.9%. International stocks rallied, with the MSCI EAFE climbing 11.8%. Bonds also rose, with the Bloomberg Barclays Aggregate Bond Index gaining 1.2%.

Outlook

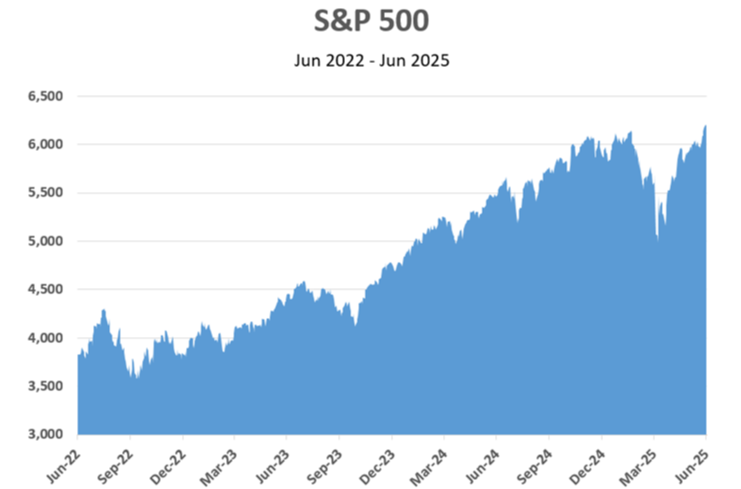

The market decline that began in February turned into a short-term collapse in the first week of the quarter. This followed President Trump’s April 2nd “Liberation Day” tariff announcement that threatened to raise the average tariff rate on imports from about 3% to near 30%. The market’s reaction was swift as the S&P 500 dropped more than 12% in just four trading sessions. Then, following an announcement that the majority of these tariffs would be paused for 90 days to allow for negotiations, the market responded with a massive single day rally that boosted the S&P 500 by 9.5%. This ranks as the 9th largest single day percentage gain in history for the index. For the month of April, the S&P 500 fell -0.7%. The rally that began in mid-April continued through May and June as the S&P 500 rose 6.3% and 5.1% respectively, bringing the gain for the large cap index to 10.9% for the second quarter.

*This graph is not intended to recommend any investment or investment activity.

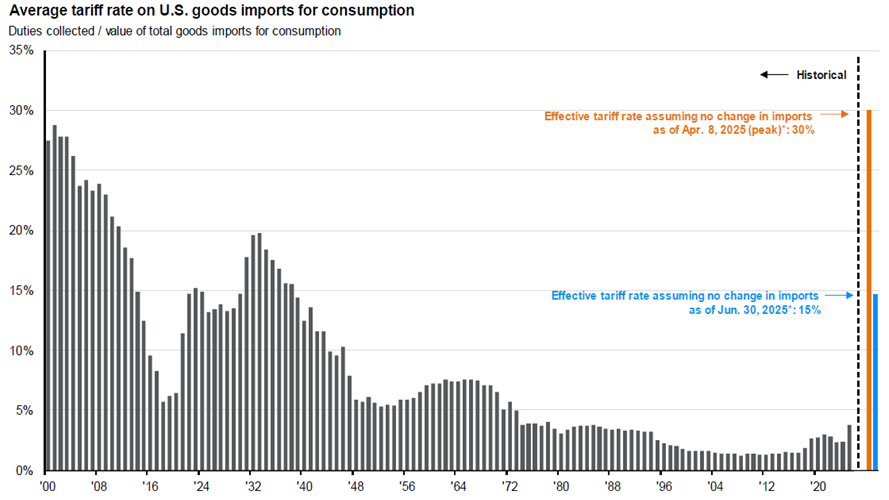

Trade negotiations have progressed slowly and investors have gradually relaxed as the worst case scenario of a large scale trade war appears to be off of the table, at least for the time being. As of this writing, the initial 90-day pause has been extended to the end of July to allow more time for negotiations with our trade partners who have not yet reached agreements with the U.S. Given the recent rise of the market to new all-time highs, it appears that the expectation among investors is that the pauses will continue for as long as necessary to allow time to reach agreements with our major trade partners.

*Source: JPMorgan. This graph is not intended to recommend any investment or investment activity.

As the chart above indicates, if there are no further changes to existing policy, the average tariff rate would settle at around 15%, which is lower than the 30% threatened on “Liberation Day,” but still much higher than the previous 3% average.

A positive change for investors this year has been that the breadth of the market has improved quite a lot. The tech sector and “Magnificent 7” are still doing well, but so are many other areas of the market, especially international stocks, with the MSCI EAFE climbing 19.5% year to date through the end of the quarter versus 6.2% for the S&P 500. The performance of international stocks for U.S. based investors has benefitted from weakness in the U.S. Dollar versus other currencies. On average, the U.S. Dollar has declined about 11% this year versus other developed country currencies.

Unpredictability has become a cornerstone of President Trump’s negotiation strategy, and so far, this approach appears to be working in his favor. However, ongoing uncertainty in policy is making it very difficult for business leaders to plan for the future. Despite this uncertainty, the economy has remained surprisingly resilient. There has been softening in some of the data, such as industrial production and consumer sentiment, but overall, the economy has remained strong, with little indication thus far of an imminent recession. Unemployment remains low at 4.1%, inflation remains relatively mild at 2.7%, and GDP is expected to have grown at an annualized rate of 2-3% in the recent quarter.

A significant accomplishment of the Trump administration has been the passage of a sizable tax and spending bill named the “One Big Beautiful Bill.” The key benefits of this bill are the extension of the 2017 tax cuts, which make the current estate tax exemption permanent, an increase in the state and local tax (SALT) deduction to $40,000, and tax cuts for income from Social Security, tips, and overtime pay. To help pay for these tax breaks, the bill includes spending cuts for Medicaid, green energy subsidies, and food benefits for poor families. Despite these spending cuts, the bill is expected to add more than $3 trillion to the national deficit over the next decade.

The potential for weaker economic activity and higher inflation caused by increased tariffs has put the Federal Reserve in a difficult situation. President Trump has made no secret about what he would like the Fed to do; lower rates now. However, Fed President Jerome Powell fears that lowering rates while the economy is performing well may lead to higher inflation. At the same time, the Fed does not want to wait too long to lower rates if the economy begins to falter. The expectation now is that the Fed will not cut rates until there is clear evidence that the economy is weakening. Most think a rate cut will not come until the fall, at the earliest.

The second quarter saw increased geopolitical concerns as the U.S. surprised the world by preemptively bombing a key nuclear facility in Iran. There also appears to be no end in sight for the war between Ukraine and Russia. So far, investors have taken these developments in stride and the market has remained relatively calm.

We begin the second half of the year facing a host of political and economic cross currents. Trade wars, major domestic policy changes, and serious geopolitical conflicts have created a great deal of uncertainty in the markets. There has been a notable uptick in volatility, but as of this writing, most stock indexes are close to their all-time highs. For the remainder of the year, we expect more of the same; increased volatility in a slowly rising stock market and economy.

Thank you very much for your continued confidence in our service and advice. If you would like to discuss our opinions, outlook, or your portfolio in greater detail, we would be happy to schedule a meeting or a conference call at your convenience. Lastly, don’t keep us a secret. If you know someone who would like help planning for their financial future, we would be pleased to speak with them to see if we can assist.