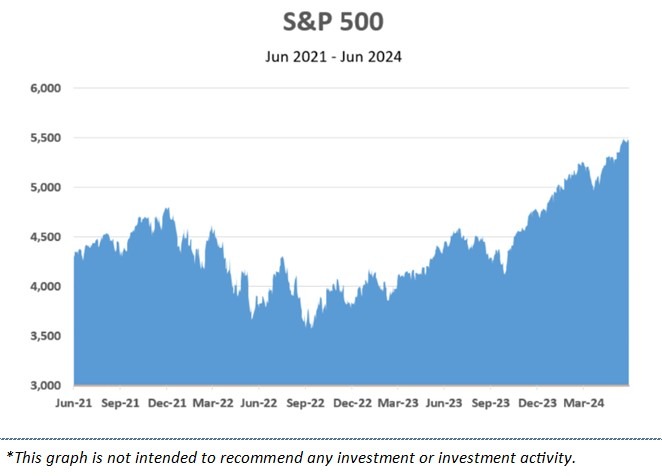

Market Recap

By most measures, 2024 has been a pretty good year for investors thus far. For the quarter, U.S. stocks rallied with the S&P 500 gaining 4.3%. International stocks fell slightly, with the MSCI EAFE losing –0.4%. Bonds rose modestly, with the Bloomberg Barclays Aggregate Bond Index returning 0.1%.

Outlook

For the year to date, the S&P 500 has gained 15.3% and international stocks, as measured by the MSCI EAFE have risen 5.3%. Bonds, however, continue to struggle as the Barclay’s Aggregate Bond Index has fallen -0.7%, and small cap stocks, as measured by the Russell 2000 Index, have risen a modest 1.7%.

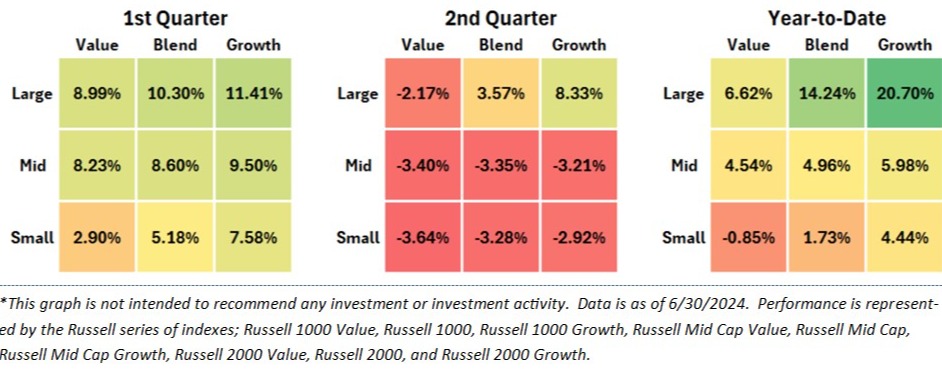

When you look a little closer, however, the gains in the market remain unusually narrow in scope. Since last year the market has been dominated by a small group of technology stocks dubbed the “Magnificent Seven” or “Mag 7.” This group is made up of Meta Platforms, Apple, Amazon, Alphabet, Microsoft, Nvidia, and Tesla. In the first quarter, gains appeared to broaden somewhat to other areas in the market. But in the second quarter, the “Mag 7” charged ahead to lead once again, leaving most of the market behind.

The chart on the next page highlights this point. The “style boxes” for each period show the index performance of subsets of the U.S. stock market, ranging from large companies to small, and steady value companies to high flying growth sectors, such as technology. The “Mag 7” are represented in the upper-right hand section of these boxes, which are large, growth oriented stocks. You can see that in the 1st quarter, gains were spread fairly evenly across the various regions in the market. In the second quarter, however, these gains narrowed tightly into the large growth area of the market. Every segment of the market, except large growth and large blend, experienced losses in the second quarter, and year-to-date, large growth leads most of the rest of the market by more than 10%.

The growth of the “Mag 7” so far this year has been 33%, while the rest of the 493 S&P 500 stocks have risen only 5%. Enthusiasm about the future of artificial intelligence has been the primary driver of the “Mag 7’s” exceptional run. The star performer of the “Mag 7” this year has been Nvidia, which has risen 149% and eclipsed a market value of over $3 trillion, briefly making it the most valuable company in the world.

Collectively, the “Mag 7” now makes up 31% of the value of the S&P 500. So if your portfolio isn’t allocated at least a third in these stocks (and at least 6% in Nvidia) your portfolio has most likely underperformed “the market.”

By design, our clients’ portfolios are far more diversified. Owning large cap growth companies is an important component, but in our opinion (and most financial research would agree) diversifying among many different types of investments is important to long-term investment success. One of the infrequent consequences of being well diversified is that at times, it requires limits on exposure to sometimes hot segments of the market.

Overall market gains continue to be helped by improving investor sentiment and ongoing evidence that growth in the economy remains strong. The recent employment report showed unemployment at 4.1%, which remains near historic lows, and GDP growth is expected to be 1-2% for 2024, with little indication that there is a risk of a recession in the foreseeable future.

Inflation continues to trend lower at a moderate pace. The Federal Reserve remains reluctant to begin cutting interest rates too soon so as to avoid another bout of inflation. The opposing concern is that waiting too long to cut rates may increase the risk of causing a recession with an overly restrictive monetary policy. The consensus at the beginning of the year was that the Fed would implement three to four rate cuts in 2024. However, with the economy showing strength, and inflation declining more slowly than expected, most now think the Fed may only cut once this year, possibly during their upcoming September meeting.

Bond rates have inched up since the beginning of the year, and mortgage and consumer lending rates remain elevated compared to pre-pandemic levels. Lending rates are likely to move lower once the Fed begins to lower rates. This will be a welcome relief to mortgage borrowers and consumers who have seen borrowing cost skyrocket in recent years.

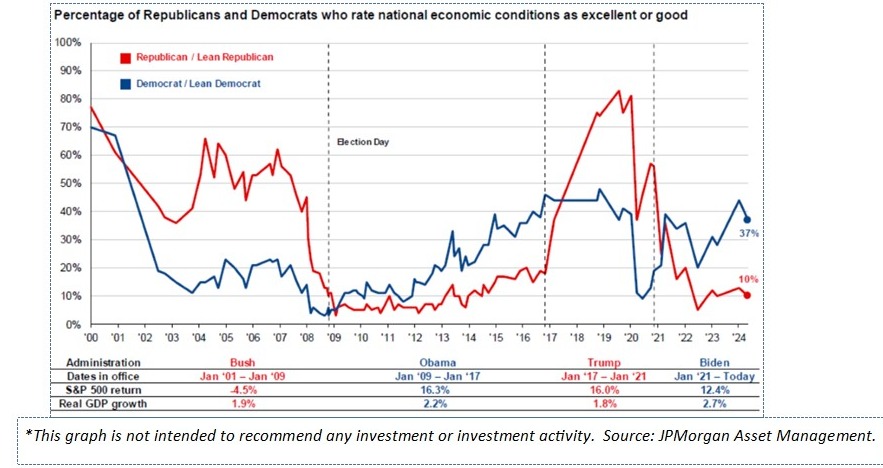

As we enter the second half of the year, we are now just a few short months from the Presidential election. This is sure to stir up investor emotions and politically colored opinions about the economy and the stock market. As the chart below illustrates, partisan leanings have a significant influence on investor opinions about the economy. The chart also shows that the market tends to follow growth in the economy, and the economy is affected by many factors, most of which are far more consequential than who resides in the White House.

Entering the second half, we are cautiously optimistic that market gains will eventually broaden to other (non-large cap tech) areas and we will see the market continue to rise through the end of the year. However, there remain many catalysts for volatility, including ongoing geopolitical tension and the upcoming Presidential election .

Thank you very much for your continued confidence in our service and advice. If you would like to discuss our opinions, outlook, or your portfolio in greater detail, we would be happy to schedule a meeting or a conference call at your convenience. Lastly, don’t keep us a secret. If you know someone who would like help planning for their financial future, we will be pleased to speak with them to see if we can assist.