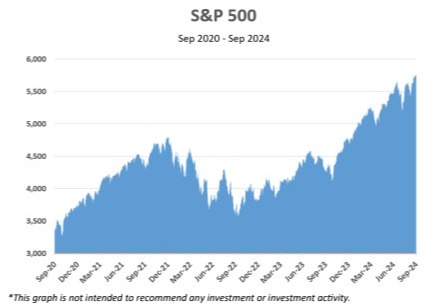

The third quarter added to what has become a very strong year in the market. Year-to-date, the S&P 500 has risen 22.1% and is up an impressive 36.4% for the past 12-months. But it has not just been large cap blue chip companies that have gained, international stocks as represented by the MSCI EAFE are up 24.8%, and even bonds, as represented by the Bloomberg Barclay’s Aggregate Index are up 11.6% over the past year. For all of the widespread volatility and negative returns in 2022, the past two years have been very good for investors.

The difference in this quarter versus the first half of the year is that gains have broadened out to more segments of the market. In recent commentaries, we’ve described how a small handful of mega-cap technology companies dubbed the “Magnificent Seven” have delivered most of the positive returns in the market. In the third quarter, value stocks and small cap stocks led market returns, with the Russell 1000 Value Index returning 9.4% and the Russell 2000 Small Cap Index returning 9.3%, versus 3.2% for the Russell 1000 Growth Index.

A significant catalyst for this shift is likely the anticipation and implementation of the Federal Reserve changing course on their monetary policy. In 2022, the Fed began to rapidly increase interest rates in a bid to cool rising inflation. As inflation has returned to more normal levels (more on this later), the Fed has shifted its focus to limiting the damage caused to the economy by higher rates. Last month, in a widely expected move, the Fed lowered interest rates by 0.5%, taking pressure off of lending rates and easing fears that higher rates would eventually lead to a recession.

As we approach the upcoming election, there are conflicting messages from both sides about the current state of the U.S. economy. This has led to a widespread misperception that the economy is in bad shape. From our perspective, this is not the case at all. The metrics most would point to as indicators of the health of the U.S. economy are GDP, unemployment, and inflation. Below is our viewpoint on each.

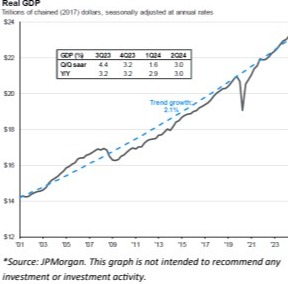

GDP—Growth in U.S. GDP has been very strong and the level of output by the U.S. economy has never been higher. Despite many predictions over the past few years to the contrary, there has not been a recession since the pandemic, and most strategists do not see the risk of an economic downturn anytime soon. Strength in wages and consumer spending has helped carry the economy to its recent highs. The current reading on the economy has GDP growth of 3% after inflation, with expectations of growth for the coming year to be around 2-3%.

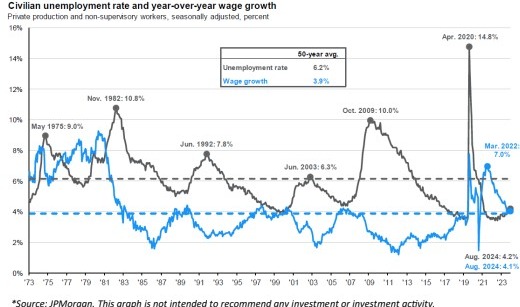

Unemployment—As of the August report, unemployment was 4.1% which is very close to all -time lows, and well below the 50-year average of 6.2%. Unemployment has stabilized around 4% for the past two years after declining from the pandemic peak of 14.8%. Given the low unemployment rate and high wage growth, it is a great time to be a U.S. worker.

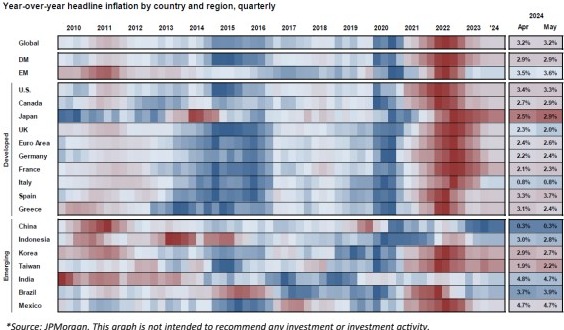

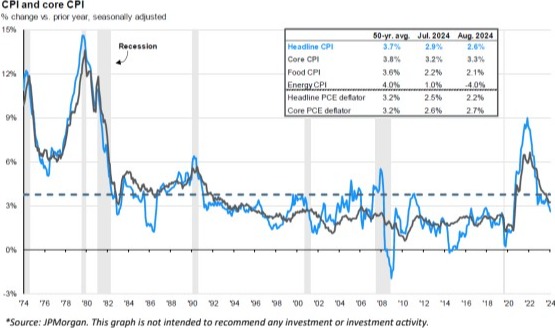

Inflation—While inflation ran high in 2022, this was a global phenomenon, brought about primarily from supply disruptions that occurred during and after the pandemic. Recall that China severely limited their economic output and exports to control the spread of COVID, and ports in the U.S. had strikes and delays relating to the pandemic response. Disruptions like these created scarcity in many products (autos for instance) that led to higher prices. As the first chart below shows, inflation was an issue for nearly every country in the world. The U.S. was neither the cause nor the sole-victim of this global problem. You can see in the second chart that inflation peaked at around 9% in 2022 and has since declined to 2.6%, which is below the 50-year average of 3.7%, and far below the high of nearly 15% in 1980.

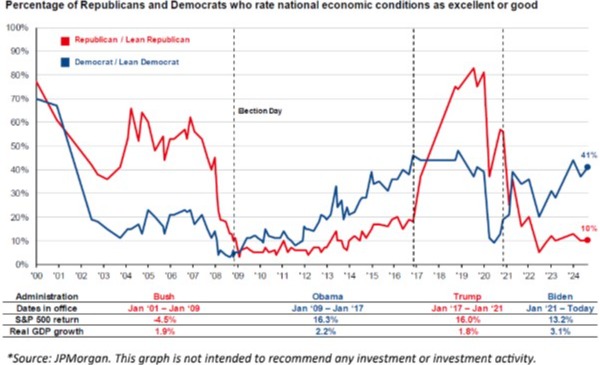

It is our assessment, and that of many economists, that the U.S. economy is in great shape at the moment. Emotions can run high during political periods, such as the run up to a presidential election. Please don’t let political leanings interfere with your long-term investment strategy. In fact, there is great danger to your financial future in allowing your emotions about election outcomes to guide your investment decision making. Below are two of our favorite graphs that illustrate this point. The first shows how polarized opinions are about the health of the economy based on who occupies the White House.

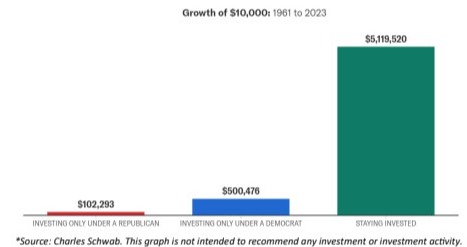

The next graph demonstrates the importance of sticking to your investment strategy, regardless of which party is in power. According to this graph, $10,000 placed in the S&P 500 in 1961, and only invested while a Republican was president, would have grown to $102,293 in 2023. If the same strategy were followed, but for Democratic presidents instead, that investment would have grown to $500,476. However, if the money were invested the entire time, regardless of who was president, that $10,000 investment would have grown to over $5.1 million! All politics aside, we think the best strategy is to remain invested.

In summary, we think the U.S. economy remains in pretty good shape. Once we get through this political season and into next year, we’re optimistic that the economy will continue to grow and that markets will continue to climb. However, there remains plenty of catalysts for near-term volatility, not least of which is the growing conflict in the Middle East and the on going war in Ukraine. There is also the risk of the unknown that can always flare up. As al ways, our advice is to settle on an investment plan that makes sense for you and your situation, and stick to it whether the market is calm and rising, or choppy and trending lower.

Thank you very much for your continued confidence in our service and advice. If you would like to discuss our opinions, outlook, or your portfolio in greater detail, we would be happy to schedule a meeting or a conference call at your convenience. Lastly, don’t keep us a secret. If you know someone who would like help planning for their financial future, we will be pleased to speak with them to see if we can assist.