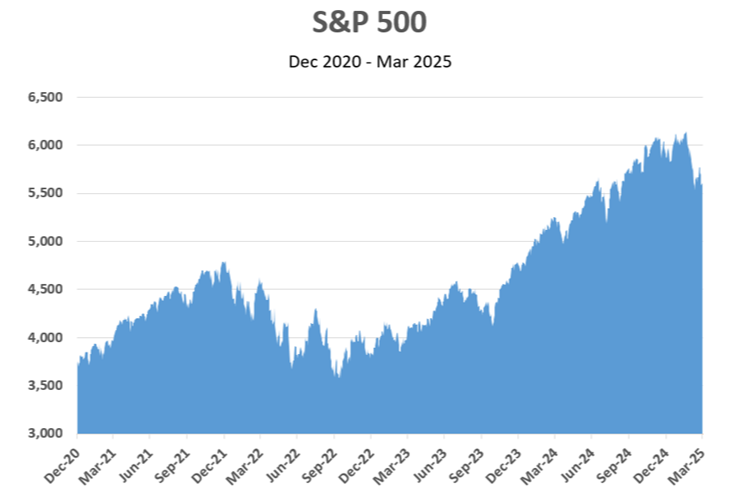

The quarter began on a positive note, with the S&P 500 gaining 2.8% in January. The gains continued for the first part of February, reaching a new all-time high before reversing course mid-month when President Trump began to threaten steep increases in tariffs on our trade partners (more on this to follow). February ended the month down –1.3%. As additional trade threats emerged in March, losses in the market accelerated and the month finished –5.6% lower, bringing the overall return for the quarter to –4.3%.

*This graph is not intended to recommend any investment or investment activity.

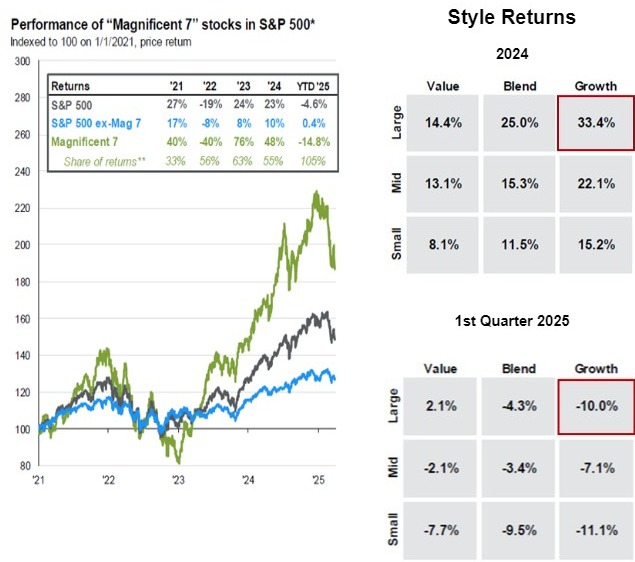

Following two very strong years in the stock market, a pullback of some sort was not surprising. The rally off of the 2022 lows has been mostly steady, and stock valuations have risen to historically high levels. Beyond the broader pullback, the new year has ushered in a significant change in market leadership. The technology-focused “Magnificent 7” lagged the market in the quarter, returning –14% for the quarter, versus 0.4% gain for the rest of the S&P 500 (see graphs on following page). Value oriented U.S. stocks and international stocks led the way as focus moved away from large cap growth stocks and the “Mag 7,” rewarding those with well-diversified portfolios.

*These graphs are not intended to recommend any investment or investment activity. Data as of 3/31/2025. Source: JPMorgan

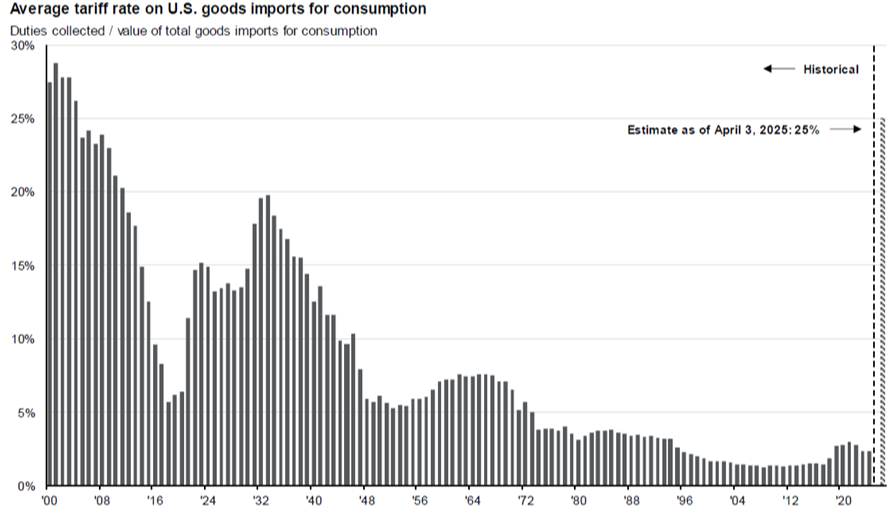

The relatively minor increase in volatility and uncertainty that began in the first quarter has been overshadowed in recent days by the surprise announcement of much larger than expected tariffs on our foreign trade partners. The “Liberation Day” announcement by President Trump raised the average tariff rate on imports from roughly 3% to 25% (see graph below). This represents the most restrictive trade policy by the U.S. in over a century. This sudden and unexpected escalation led to the steepest drop in the stock market since the 2020 COVID-19 crisis, wiping out nearly $6 Trillion in market value in just two trading sessions. As of this writing, the S&P 500 has declined –19% since the mid-February peak, threatening a bear market for the index. The tech-heavy Nasdaq and small cap Russell 2000 Index have already entered bear market territory.

*This graph is not intended to recommend any investment or investment activity. Source: JPMorgan

These tariffs have been pitched by the President as a way for the U.S. to level the playing field in global trade, punishing our trade partners for years of unfair practices. However, the cost of these tariffswill ultimately fall on the shoulders of American consumers. The Wall Street Journal editorial board recently cited these tariffs as amounting to the largest tax increase on American households in history, with revenue from the tariffs expected to reach $6 Trillion over the next 10 years. The increased costs for imported goods will ultimately be passed down to consumers, making many consumer products more expensive and driving up inflation an estimated 2-3% from current levels.

The consensus among investment strategists is that there are obvious near-term consequences of this trade war, namely higher prices and lower economic growth among the most impactful. Longer-term, if these trade restrictions persist, there could be many unintended consequences, similar to the years that followed the trade disruptions caused by the COVID-19 crisis. Global supply lines are intricate and sensitive to disruptions. Most products with any complexity, such as automobiles and household appliances, rely on a multitude of components, imported from multiple countries. There is also the risk of the country losing its leadership position in the global economy, namely to China and the Euro-zone, who could seize the opportunity to increase their output as more stable and trustworthy trade partners.

The hope of the Trump administration is that by implementing these extreme and punitive measures, our global trade partners will be motivated to negotiate more favorable trade agreements with the U.S., setting the country up for a more beneficial global trade environment in the future. The risk is that countries could choose instead to retaliate, escalating an already difficult situation. Following the announcement of these tariffs, Vietnam has offered to negotiate much more favorable terms, while China, on the other hand, announced retaliatory tariffs, raising their tariff rates for goods imported from the U.S. to 34%, matching the tariff rate we’ve imposed on their imports. As of this writing, we are very early in this crisis, and time will tell how things will play out.

The potential double-whammy of higher inflation and weaker economic growth place the Federal Reserve in a precarious position. Coming into the year, the Fed planned to lower their benchmark interest rates 2-3 times this year. If inflation begins to rise, they may be forced to pause their plans to lower interest rates and perhaps even raise rates in an attempt to calm inflation. At the same time, the likelihood of a recession has increased dramatically, which may require the Fed to lower rates to stimulate the economy. If inflation is too high and at the same time the economy is weakening, the choice to raise or lower interest rates from current levels may become extremely difficult.

At the beginning of the year, most economists and strategists felt the economy was on solid footing. GDP was expected to rise 2-3%, unemployment was expected to remain around 4%, and a recession appeared unlikely. With recent developments, the consensus view is now that a recession this year is likely. How deep and how long will depend on the severity of this trade war, and the difficulty in restoring normalcy in global trade.

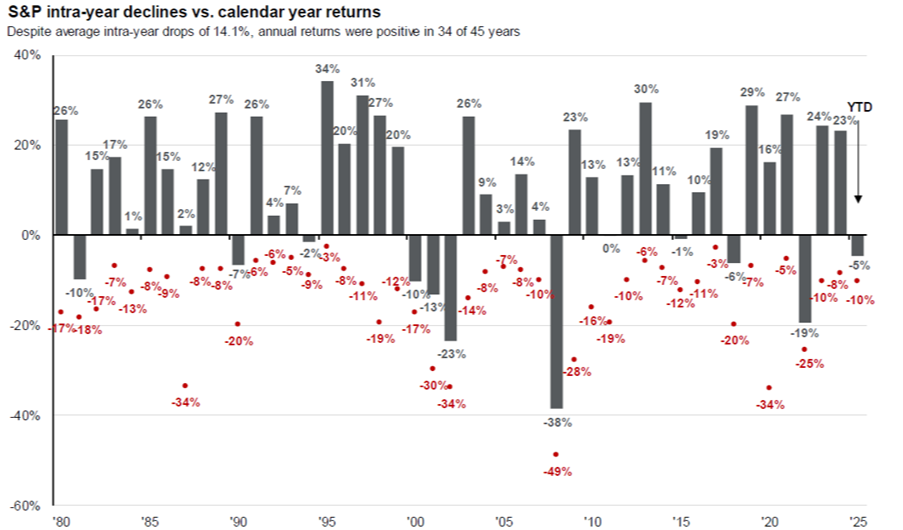

Although the recent market decline was quite sudden, pullbacks of this magnitude occur with some frequency. As the chart below shows, over the past 45 years, the market has experienced an average pullback of -14.1% each year, but despite these pullbacks, the market has been positive in 34 of those 45 years.

*This graph is not intended to recommend any investment or investment activity. Data as of 3/31/2025. Source: JPMorgan

Even with significant uncertainty, the underlying strength and dynamism of the U.S. economy will likely carry us through this crisis. Although a recession suddenly seems likely, most strategists feel that cooler heads will ultimately prevail and this self-initiated trade war will prove short-lived, and any recession will be mild. U.S. companies are exceptional at adapting as business environments evolve. This will likely prove true again and American innovation will eventually lead us back to strong growth in the economy, and by extension, the stock market.

It is also important to keep in mind that our clients’ portfolios are well-diversified, including both U.S. and foreign stocks, both aggressive and defensive. The majority of our clients also have an allocation to bonds, which have done a nice job of providing protection during this downturn thus far. Our plan in the near-term is to look strategically for an opportunity to begin rebalancing back to our target allocations in the many areas of the market represented in our clients’ portfolios.

Thank you very much for your continued confidence in our service and advice. If you would like to discuss our opinions, outlook, or your portfolio in greater detail, we would be happy to schedule a meeting or a conference call at your convenience. Lastly, don’t keep us a secret. If you know someone who would like help planning for their financial future, we would be pleased to speak with them to see if we can assist.