Market Recap

For the quarter, U.S. stocks advanced with the S&P 500 gaining 2.4%. International stocks fell, with the MSCI EAFE declining –8.1%. Bonds also stumbled, with the Bloomberg Barclays Aggregate Bond Index falling –3.1%.

Outlook

For the year, the S&P 500 rose an impressive 25.0%, coming in just shy of last year’s 26.3% gain. The S&P 500 returned 20%+ in consecutive years for the first time since the late‐90’s, bringing the market to a new all‐time high in mid‐December before pulling back in the final weeks of the year.

*This graph is not intended to recommend any investment or investment activity

*This graph is not intended to recommend any investment or investment activity

For the fourth quarter, the S&P 500 gained 2.4%. The quarter began on a somewhat negative note with a –0.9% return in October as uncertainty and anxiety heading into the election caused investors to exercise caution. November delivered the only positive month in the quarter as the index rose 5.9% as investors expressed approval and optimism about the election results. December saw the index pull back ‐2.4% as year‐end profit taking sent most of the year’s winners lower.

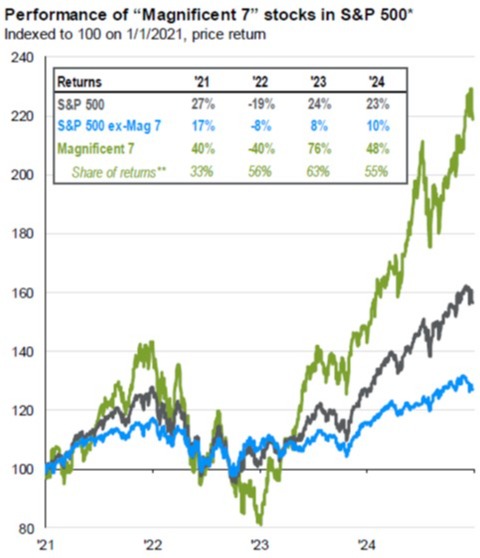

For the past two years, much of the upward momentum in the market has come from the strength of the technology sector, specifically from a select group of stocks dubbed the “Magnificent 7,” or “Mag 7.” As the following chart shows, the Mag 7 collectively rose 48% last year, compared to 10% for the rest of 493 S&P 500 stocks. The rally in the Mag 7 stocks has been so powerful, they have grown to the seven largest stocks in the U.S. and now represents about a third of the index. This is higher than the previous peak of 22% for the seven largest stocks, which occurred at the height of the late‐90’s tech‐bubble.

*Source: JPMorgan. This graph is not intended to recommend any investment or investment activity.

Much of the gains in the Mag 7 stem from tremendous optimism in advances in artificial intelligence and the adoption of this new and exciting technology. With this, valuations for these stocks have become extremely high. The same can be said for the rest of the market which sits near historically elevated levels, with the technology sector valued at 29.6 times expected 2025 earning and the rest of the index (non‐tech) valued at an average of 21.4 times expected earnings.

This places the market in a rather precarious position as we begin the new year. Valuations are approaching the highs of the late‐90’s tech‐bubble. In many ways, the euphoria surrounding the Mag 7 has been similar to the high‐flying sentiment for internet stocks of that time. There is a key difference, however; the Mag 7 companies are very profitable and have grown their earnings very rapidly. But now, as it was then, we believe it is a mistake to allocate too much of an investment portfolio into this concentrated area of the market.

Our clients’ portfolios hold many different types of investments in their portfolios; from the massive technology growth stocks of the Mag 7 to small stocks with steady and predictable businesses. They own international stocks from both developed and emerging economies. In the past month, we have been scaling back our clients’ exposure to the high flying growth areas of the market and reallocating to the less loved segments, as well as adding to fixed in‐ come for those who have balanced allocations. As it was during the tech‐bubble, we think owning a well‐diversified portfolio will prove helpful if today’s leaders in the Mag 7 tumble in a similar fashion to the technology leaders of the late‐90’s.

In addition to the Mag 7, investors are highly focused on the Federal Reserve and potential changes to key interest rates. Last year, the Fed began lowering interest rates as inflation began to cool. The progress in slowing inflation has occurred in fits and starts, and the Fed has responded in kind, reducing the number of rate cuts they expect to make next year from four to two cuts. They remain hopeful that inflation will continue to slowly decline to their long‐ term target of 2%. Although interest rates in most areas have come down from their recent peaks, they remain much higher than they were just a few years ago. This has made it more difficult for consumers to borrow money to buy homes, automobiles, and other high‐ticket items. However, higher rates have also provided better yields for investors in bonds, CD’s, money markets, and other savings instruments.

Further, investors are focused on the near‐term possibilities of a new agenda proposed by the incoming Trump administration. On the campaign trail, President‐elect Trump promised massive tariffs against many of our trade partners, mass deportations to deal with our immigration problem, and extending tax cuts from his previous administration. Each of these policies have the potential to significantly impact the economy, inflation, and the stock market. The majority of strategists believe that many of the policies proposed during the campaign will be less extreme once they are actually implemented. Additionally, a narrow majority in the house and senate could further challenge and dampen the President‐elect’s agenda as policies work their way through the legislative process. The market, up until now, has mostly shrugged off the most extreme policy changes as unlikely and responded to Trump’s successful reelection positively. We won’t really know precisely what the President‐elect has in mind until after his inauguration, but most are hopeful that cooler heads will prevail when the time comes to implement some of the proposed policy changes.

Although uncertainties exist, we begin the year with an economy that is in excellent shape. Earnings growth was 9.5% last year and is expected to accelerate to 14.8% in the coming year. Real GDP grew by 2.4% over the past year and is expected to maintain a similar pace for the foreseeable future. Unemployment remains near historically low levels with the most recent reading of 4.1% as of year‐end. Additionally, given the recent rise in real estate values and the stock market, total household net worth in the U.S. has grown to almost $160 trillion as of the 3rd quarter, up nearly $18 trillion from the previous year.

Despite the elevated valuations in the stock market, and many external risks, we think a diversified portfolio should fare reasonably well in the coming year. Returns are not likely to maintain the rapid upward pace of the past two years, but we remain optimistic that gains can continue into the coming year and beyond.

Thank you very much for your continued confidence in our service and advice. If you would like to discuss our opinions, outlook, or your portfolio in greater detail, we would be happy to schedule a meeting or a conference call at your convenience. Lastly, don’t keep us a secret. If you know someone who would like help planning for their financial future, we would be pleased to speak with them to see if we can assist.

Horizon Wealth Advisors | horizon‐advisors.com January 2025